Regional Property Market Update Spring 2022: Thames Valley

Posted on: Tuesday, April 5, 2022

Standing firm

2022 has started strongly. Sales volumes in January are predicted to be 10% higher than their long- term (2012–2021) average and, except for a year ago, are the strongest since 2007 (Dataloft, HMRC). Buyer demand remains steadfast, up 16% year-on-year (Rightmove). Property price growth continues to be sustained; annual price growth in the year to January was at its strongest in over 15 years (Nationwide). Rightmove reported the biggest monthly jump in the asking price of a newly listed property since 1994 and when asked, the majority of agents are still expecting price growth over the next three- and 12-month period.

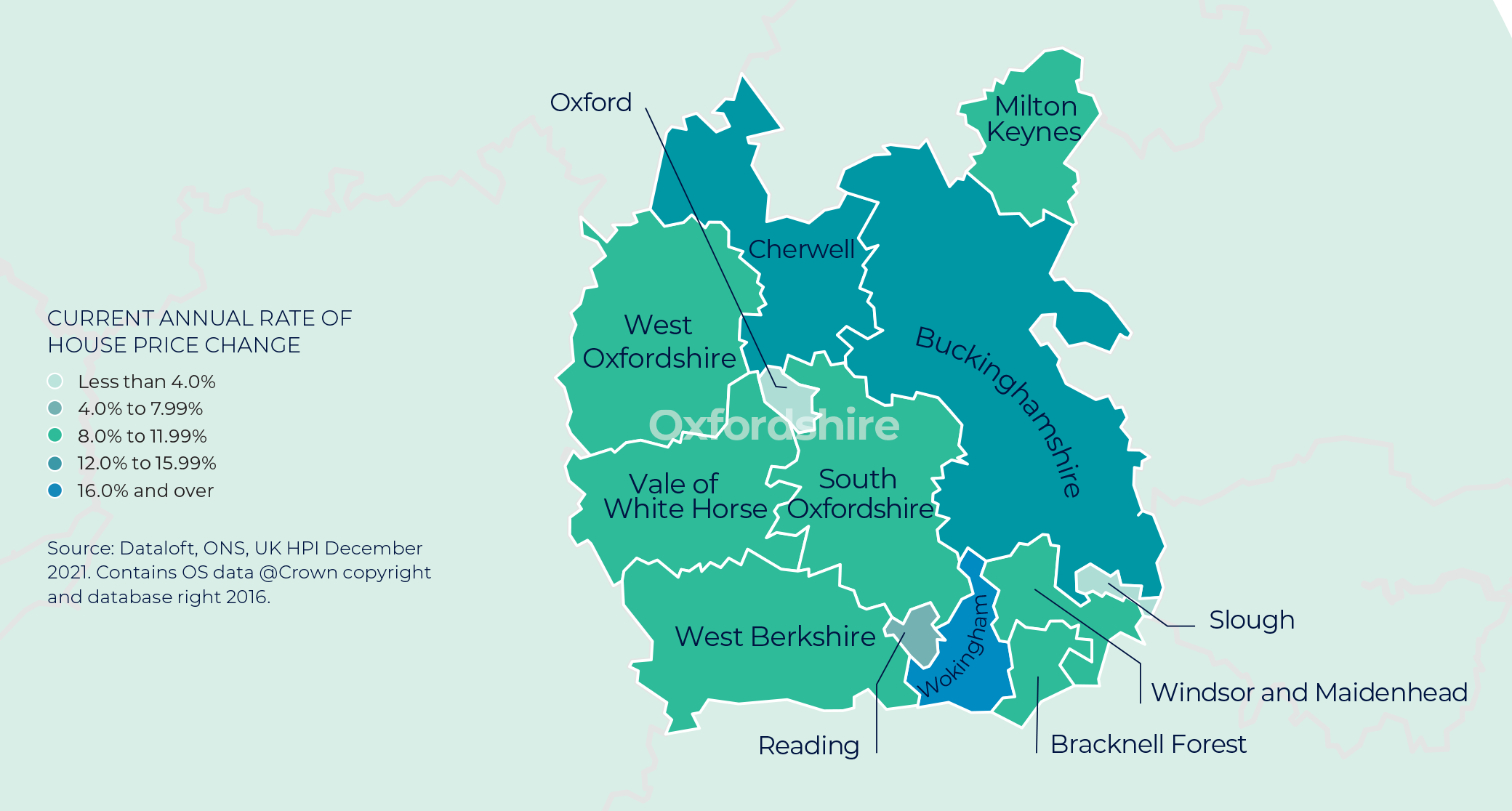

At 12.6%, annual property price growth in the South East of England is considerably stronger than the 5.1% evident a year ago. The pandemic ‘search for space’ is still playing out in many markets, with prices for detached homes currently seeing the strongest growth of all property types; average prices are up over 16% year-on-year. With office returns and hybrid working now in place, there has been renewed interest in apartment living, and many town and city centre locations are seeing a rise in buyer demand.

Winds of change

Although the quantity of property for sale remains low, with the Royal Institution of Chartered Surveyors (RICS) reporting stock levels per agent at a record low in January (barring the market closure in spring 2020), there are signs of change. New listings in January rose 11% year-on-year, with Rightmove noting a substantial rise in home valuation requests – an indication that many are looking to sell before they buy in current conditions. These should feed through to agents’ books over the coming months. Historically, March is the strongest time to sell, with the highest number of buyer enquiries per property for sale.

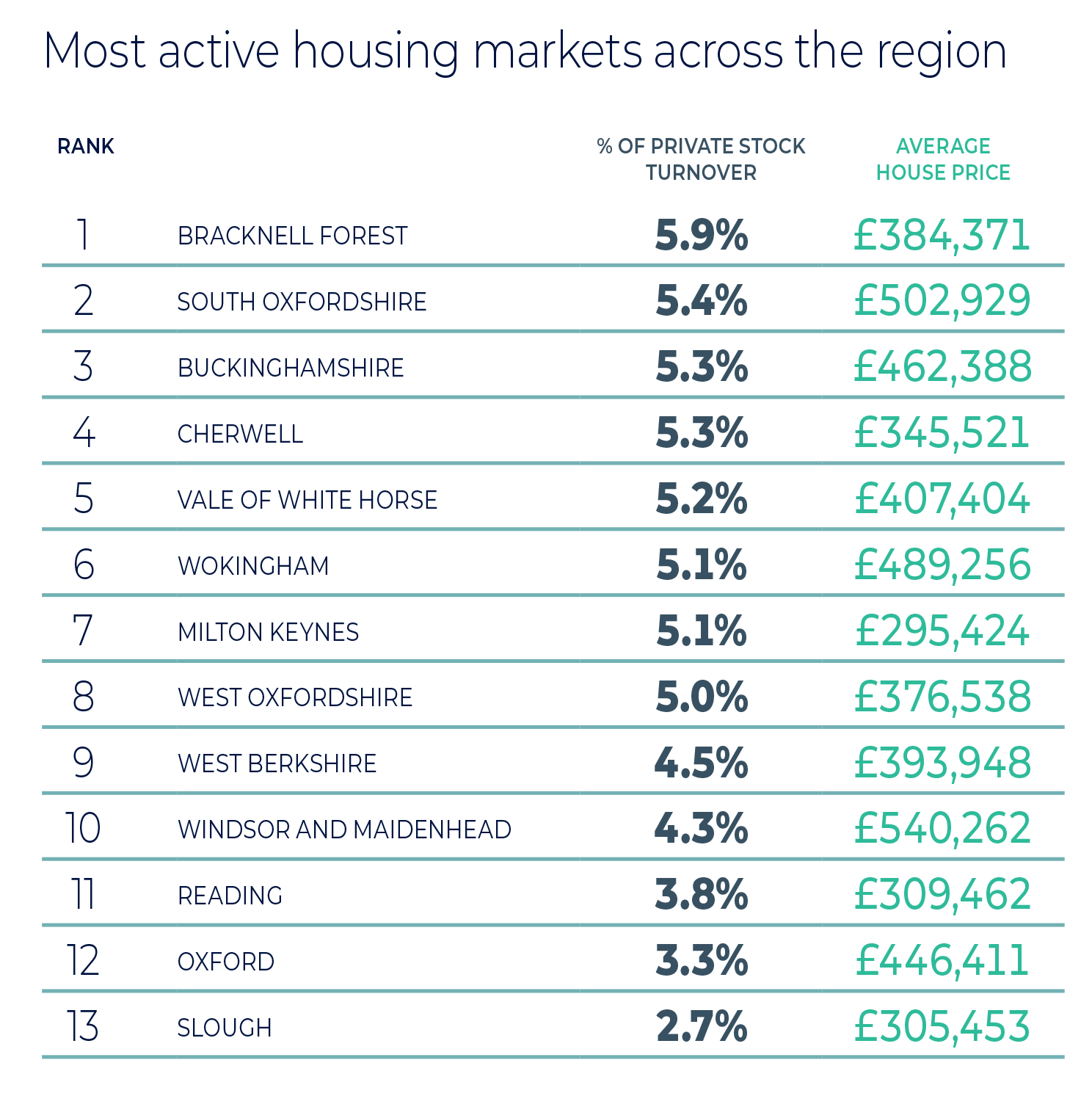

Bracknell Forest and South Oxfordshire proved the fastest-moving markets in the Thames Valley, Berkshire, Oxfordshire and Buckinghamshire over the course of 2021, with more than one in every 20 privately owned properties estimated to have changed hands. 2022 has started with momentum. At 44 days, the average time taken to sell a property in the South East is over three weeks quicker than a year ago.

Sunshine and showers

Across the UK, governments are announcing their plans for ‘living with COVID’ and hybrid working is bedding in. With economic growth of 7.5% over the course of 2021, the UK economy is close to its pre-pandemic level. However, consumer confidence remains on edge due to the rising cost of living. Increases in the cost of food and clothing, along with rising fuel and energy prices, look set to squeeze many household incomes. Savings made during the pandemic might provide a cushion in the short term, and while interest rates may well rise from the current 0.5%, they remain low by historic standards.

Properties for sale in the Thames Valley region

Chackmore, Buckinghamshire, 3 bedrooms

This rarely available 18th Century thatched cottage is nestled within the quiet and rural village of Chackmore. Chackmore is a small village situated in the North Western region of Buckinghamshire approximately 2.5 miles North of Buckingham. The Cottage is believed to be dated back to 1765 and oozes with charm and character. In brief the cottage briefly comprises an entrance lobby, lounge with feature inglenook fireplace, kitchen/breakfast room and conservatory on the ground floor. The first floor offers three bedrooms and a newly refitted bathroom. Externally the property boasts a private tiered garden with decking, outbuilding and a lovely outlook over fields to the rear.

Windsor, Berkshire, 2 bedrooms

This beautifully presented two-bedroom semi-detached period cottage is located on a quiet residential road within walking distance to Windsor Town Centre with its mainline rail links and shops, bars and restaurants. Featuring a south-facing garden with side access and separate log cabin, the property further benefits from a double reception room, high ceilings throughout and potential for a second story extension and loft conversion (STPP).

Wooton Village, Oxfordshire, 3 bedrooms

This lovely period cottage is the very epitome of country living, offering an idyllic village setting combined with ready access to Oxford. Believed to be over 400 years old, Vine Cottage is tucked away in a peaceful location overlooking the village green. Carefully refurbished by the current owners the flexible accommodation now comprises a modern open-plan kitchen and dining area with log-burning stove, a separate utility room, a sitting room also with log-burner as well as underfloor heating beneath the stone-flagged floor, a study or fourth bedroom, and a downstairs bathroom with feature roll-top bath. Upstairs are three further bedrooms with an additional toilet/shower room.

Contact us

As property prices and demand continue to rise, sell your property with experts in the property industry this spring. Contact your local Guild Member today.